Our clients receive regular updates from us regarding interesting, useful and often crucial information, to ensure their business runs as smoothly as possible.

View the full February 2021 Client E-news.

GET READY FOR YEAR-END

Before you say goodbye to the 2021 financial year, make sure you work through a year-end process to ensure you maximise your tax deductions and minimise your tax bill. Here are the must-do items:

Assets

- Assets purchased prior to 17 March 2020 and costing $500 or less should be expensed. Assets purchased after this date, but before 17 March 2021 and costing $5,000 or less can be expensed. Assets purchased from 17 March 2021 and costing less than $1,000 can be expensed.

- Claim depreciation from the first day of the month of purchase.

- Ensure assets traded in are disposed of and the replacement asset depreciated at its full cost.

- Depreciate residential rental property chattels purchased during the year.

- Claim depreciation on commercial property from 1 April 2020.

- Ensure assets sold, stolen, scrapped, destroyed or no longer used are removed from the asset register and loss on disposal calculated.

- If an asset sale is expected to result in depreciation recovery, consider deferring the sale until after 31 March.

- Ensure deductible feasibility and R&D costs have been expensed.

Trading Stock

- Value closing stock at market selling value if lower than cost.

- Carry out a stocktake 31 March to ensure an accurate closing stock figure.

- Write-off obsolete stock.

- If trading stock is less than $10,000, and turnover is less than $1.3m, use opening stock value as closing stock figure.

Accruals and Provisions

- These are not deductible in the current year unless you are definitively committed to the expense at year-end and the amount can be reliably estimated.

- Keep a record of employment provisions paid out between 1 April and 2 June as that portion of the provision is deductible at 31 March.

Repairs and Maintenance

- A one-year warranty purchased with a fixed asset can be deducted as an expense rather than capitalised providing the cost of the warranty can be separately identified.

- Review fixed asset registers to ensure genuine R&M has been expensed and not capitalised to fixed assets.

- Consider carrying out R&M work before year-end.

Bad Debts

- The debt must be physically written off the debtors’ ledger by 31 March to be deductible.

- Retain documentation to support the debts as not recoverable.

- Claim the GST adjustment.

Prepaid Expenses

- Some expenses paid in advance (eg, rent, insurance, advertising, service contracts and subscriptions) can be tax-deductible in the current year if not treated as a prepayment in the accounts.

- ACC levies are deductible when paid.

Donations

- Cash donations paid to donee organisations or registered charities are deductible up to the level of net income. If the business is in a tax loss position, consider the owner making the donation and claiming the donation rebate.

Cut-off

- Follow year-end cut-off procedures to ensure sales, stock, expenses etc are accounted for in the correct year.

Shareholder Matters

- Consider paying a dividend or shareholder salary if there is an overdrawn shareholder current account.

- Check the company has sufficient imputation credits; consider bringing forward a tax payment if necessary.

- Dividends for the 2020-21 year should be paid or credited before 31 March 2021.

- Dividend withholding tax is payable on 20 April 2021.

- Review shareholding changes throughout the year to ensure shareholder continuity has been maintained.

- If a dividend is being paid to a non-resident, non-resident withholding tax may need to be considered.

International Matters

- Interest deductibility may be impacted by the thin capitalisation rules if there is control by a non-resident or offshore investment.

- Cross-border related party transactions need to be at an arm’s length price or will be at risk of being restated by the IRD under the transfer pricing rules.

Income Tax

- The third instalment of 2021 provisional tax is due 7 May 2021 based on actual results to 31 March so it is important to have your records in order to determine this.

- If you wish to use the AIM provisional tax method, you must be using the correct accounting software by 1 April 2021.

- If you have not yet filed your 2020 income tax return, ensure it is filed by 31 March otherwise late filing penalties will be charged, your extension of time to file 2021 may be lost and the 4-year statute bar periods extends a further year.

- A loss offset subvention payment for the 2020 income year must be paid by 31 March 2021.

Look-through companies

- If you want your company to enter or exit the look-through company regime for the 2021-22 income year, the election notice needs to be filed by 31 March 2021.

GST

- Where assets are used for both business and private use, make your year-end GST apportionment adjustment in the 31 March GST return.

In summary, putting aside time to consider the above before you race into the new financial year will help ensure you maximise your tax deductions for 31 March 2021 and ultimately lower your tax bill.

__________________________________________________________________________________________________________________________

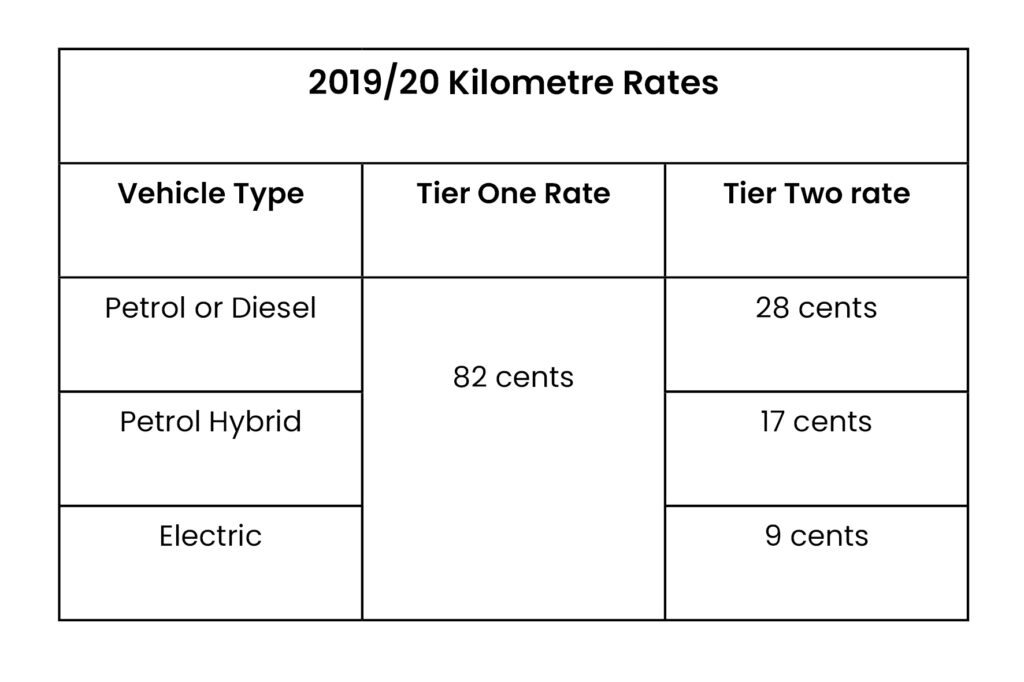

IRD 2020 KILOMETRE RATES

In December IRD released the kilometre rates for the 2019/20 income year.

If the 2020 tax return has already been filed, a request can be made to amend the tax return for the new rates however the cost benefit of doing so should be considered first.

Kilometre rates for employee reimbursement

When an employee uses their private vehicle in their employer’s business, the employer is able to pay the employee a tax-free reimbursement for the actual costs of the business use of the vehicle. As this can be difficult to quantify, employers typically base the reimbursement on the IRD’s kilometre rates.

If the employee keeps a logbook, the Tier One rate applies to the first 14,000 km of business use in an income year. For business use in excess of 14,000 kms, the Tier Two rate applies based on the type of vehicle. If the employee doesn’t keep a logbook, the Tier One rate is limited to the first 3,500 kms of business use, with the Tier Two rates used for kilometres in excess of 3,500. Given these thresholds need to be determined, a logbook should be maintained anyway.

Kilometre rates for self-employed and close companies

When a person uses a motor vehicle for both business and private purposes, they can be reimbursed for the cost of the business use. Business use can be determined by either using actual costs, or keeping a logbook and using the IRD’s kilometre rates. The method chosen needs to continue to be applied to the vehicle while it is used for business use.

When the kilometre rate is used, no additional deduction for depreciation can be claimed as it has already been factored into the kilometre rates.

As for employee reimbursements, when a logbook is kept, the Tier One rate applies to the first 14,000 km of business use, and the Tier Two rates apply for business use in excess of 14,000 kms. When a logbook is not kept, again the Tier One rate is limited to the first 3,500 kms of business use, with the Tier Two rates used for kilometres in excess of 3,500 kms.

__________________________________________________________________________________________________________________________

REINTRODUCTION OF THE 39% TOP PERSONAL TAX RATE

From 1 April 2021, individuals earning over $180,000 pa will be paying 39% tax on income in excess of $180,000.

It is good practice to review your business and investment structure regularly to ensure that it is still fit-for-purpose. Changes in legislation are often a prompt to review your current structure and reflect on any changes in circumstances that may deem some future-proofing is required.

At the very least, closely-held companies should be considering the level and timing of their year-end dividend to ensure it is completed before 31 March 2021, bearing in mind available imputation credits and the cashflow impact of the RWT.

__________________________________________________________________________________________________________________________

WINDOW FOR LOW-VALUE ASSETS ABOUT TO CLOSE

The opportunity for business owners and landlords to take a full tax deduction for new assets costing $5,000 or less is rapidly disappearing.

The temporary increase in the low-value asset threshold from $500 to $5,000 will end on 16 March 2021, at which time the threshold will reduce to $1,000.

The Government introduced the temporary increase as part of their Covid support measures back in March 2020. The increase resulted in taxpayers being able to claim a tax deduction for asset purchases of $5,000 or less. Previously purchases over $500 had to be capitalised, and if depreciable, expensed over the life of the asset. In the case of non-depreciable items, such as building improvements to a residential rental property, no tax deduction was allowed.

While the low-value asset threshold applies to all taxpayers, it is particularly relevant for residential property landlords considering undertaking improvements to bring their property in line with the Healthy Homes Standards. If this is you, look to undertake the improvements before 17 March 2021 as the purchase of items to meet the new Healthy Homes Standards, such as new insulation, heat pumps, opening windows, and extractor fans that cost $5,000 or less are now able to be fully expensed if paid for on or before 16 March 2021.

Don’t leave the improvements until after 16 March 2021 when the deduction threshold drops down to a meagre $1,000.

__________________________________________________________________________________________________________________________

Any questions?

If you have questions about any of the above, please do not hesitate to contact us on (09) 470 0444.